Your crew buys fuel en route, picks up materials mid-job, and fixes equipment on the spot. By the time statements arrive, you’ve lost the connection between expenses and the work behind them. That disconnect is what pushes owners and fleet managers to look for the best credit cards for construction and contractors.

You’re not chasing rewards. You’re trying to track spend by vehicle and job site, and control who can spend, where, and on what. Most credit cards for contractors weren’t designed for this.

They struggle with fuel, maintenance, and multi-vehicle cost tracking. But some were designed for this. You just have to know where to look.

Here you’ll find the seven best credit cards for construction, ones that are built to reduce admin work, improve visibility, and support how construction job site spending actually happens.

How We Chose The Best Credit Cards for Contractors and Construction Businesses

We evaluated 15+ credit cards for construction businesses, measuring how well each supports fuel, materials, equipment rentals, repairs, tolls, and job-site purchases. Rewards alone weren’t enough.

Each card had to hold up on controls, reporting, and expense workflows across multiple vehicles, crews, and vendors.

We also prioritized card acceptance, total cost, and job-level accounting clarity, the factors contractors can’t afford to get wrong.

Every card below earned its place based on these criteria.

- Controls for crews, vehicles, and job-site spending: Construction needs flexibility with guardrails. We prioritized credit cards that let you issue employee cards, set limits, and restrict spend by merchant type or category, so field purchases don’t turn into leakage. This is critical when multiple crews buy fuel and supplies without checking in with the office for every purchase. Strong controls prevent misuse without slowing work.

- Visibility and reporting: We favored construction credit cards and platforms that provide clean transaction data, real-time alerts, and reporting that supports job costing and auditing. If a card only gives you totals and vague merchant names, your team ends up rebuilding context manually.

- Acceptance where contractors shop: We favored construction credit cards with broad acceptance across fuel, parts, tolls, and maintenance. That flexibility prevents downtime and keeps crews from reaching for personal cards when routes change.

- Total cost and terms: We compared annual fees, penalty pricing, and reward caps, knowing high rewards often fall apart once limits kick in or balances carry. Practical friction mattered too. For example, we didn’t favor cards with extra fees for employee cards, restricted reporting, or clunky expense workflows.

- Integrations and workflow fit: We prioritized construction credit cards with strong construction accounting and expense integrations to reduce receipt chasing, manual coding, and month-end friction. Automation is one of the clearest ways to cut admin time as fleets grow.

The factors above guided our picks for the best credit cards for contractors. Keep reading for a practical breakdown of each card and where it makes sense for different construction needs.

The 7 Best Credit Cards for Construction

Here are the 7 best credit cards for construction that stood out to us after weeks of hands-on evaluation and comparison.

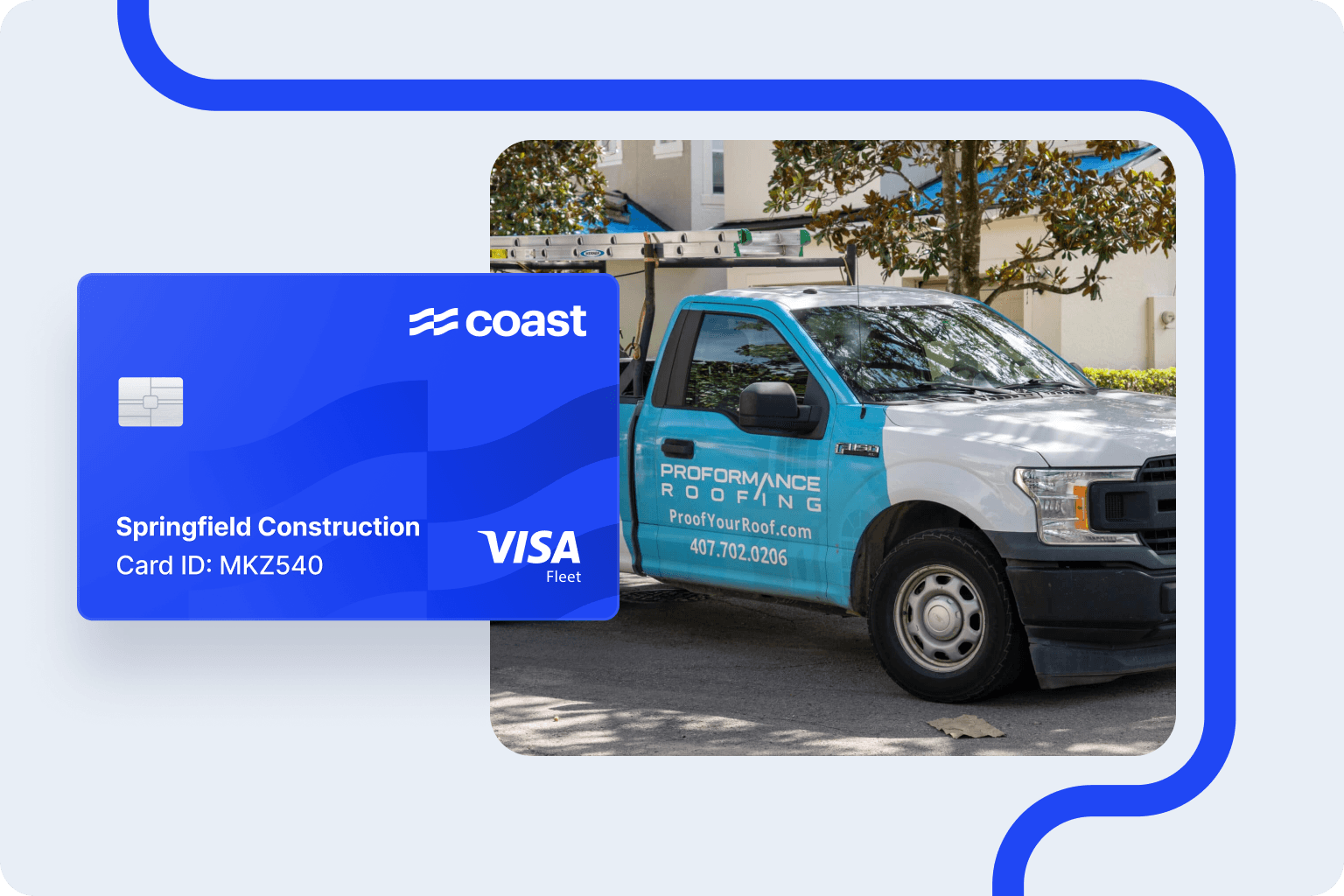

1. Coast

Coast is specifically built for trades and construction businesses that manage crews in the field, run a fleet of vehicles, and need tighter control over day-to-day spend.

Unlike traditional credit cards, Coast combines a corporate card, a fuel card, and expense management solution, instead of keeping multiple systems. Coast cards work anywhere Visa is accepted and supports all construction expenses, including fuel, maintenance, parts, and tolls.

Plus, you can earn 3-9¢ per-gallon rebates at 30,000+ fuel stations, and 1% cash back on everything else, all redeemable for travel, gift cards, cash, or towards your statement.*

With Coast’s business card for construction, you get a complete fuel card with tight controls and telematics integrations. The platform lets you connect transactions to vehicle and location data to help you spot and stop suspicious activities.

On the operations side, Coast fits cleanly into your existing construction workflows. It connects directly with accounting systems like QuickBooks, NetSuite, and Sage Intacct, as well as project management tools like BuildOps or Knowify.

Receipts, job codes, and custom fields are captured via phone, helping you tie fleet expenses to specific jobs without manual follow-up. Admins can also apply customizable controls by user, merchant category, or individual merchant. You also get flexible rewards redeemable for travel, gift cards, cash, or statement credits.

Coast offers a $25,000 annual fuel fraud guarantee that covers both employee misuse and external fraud (eligibility and terms apply).

- Complete fuel card with telematic integrations

- Captures job codes, receipts, and custom fields via phone

- Customizable controls by user, merchant category, or merchant

- Integrates with project management tools like BuildOps or Knowify

- Direct integrations with QuickBooks, NetSuite, and Sage Intacct

- Flexible rewards redeemable for travel, gift cards, cash, or statement credits

- Monthly fee of $4 per user per month

- Suits only trades, construction, and transportation businesses

- May not be ideal for businesses prioritizing very high rewards

2. American Express Business Platinum

The American Express Business Platinum Card is built for companies that put employees on the road and want travel benefits alongside business perks.

New card members can earn as high as 300,000 membership rewards points after meeting the required spend. Plus, members receive access to the Global Lounge Collection, including Centurion Lounges, Delta Sky Club visits (when flying Delta), Priority Pass Select, and select partner lounges.

You can also earn 5x membership rewards points on flights and prepaid hotels booked through Amex Travel, along with a 35% points rebate when using Pay with Points for eligible airline bookings.

There are also no foreign transaction fees. Other business perks include statement credits with Dell, Adobe, Indeed, and wireless providers, premium car rental benefits, and travel protections.

- No preset spending limit for more flexibility

- 5x membership reward points on flights and hotels booked via Amex Travel

- Attractive travel perks, with hotel and airline credits

- High annual fee

- No spend management tools or integrations with accounting systems

- Rewards by category might not suit you

- No ability to limit spending by employees

3. Capital One Spark 2% Cash Plus

The Capital One Spark 2% Cash Plus Card is ideal for businesses that don’t want to think about categories or caps. Every purchase earns unlimited 2% cash back, everywhere. Plus, new cardholders earn a $2,000 cash bonus after spending $30,000 in the first three months, with the opportunity to earn additional $2,000 bonuses for every $500,000 spent in the first year.

This is a pay-in-full charge card. The $150 annual fee is refunded in any year you spend at least $150,000. Beyond cash back, the card offers 5% cash back on hotels and rental cars booked through Capital One Business Travel, along with no foreign transaction fees.

Plus, you get tools for managing team spend, like free employee and virtual cards, customizable spending limits, detailed transaction data, year-end summaries, and easy downloads for accounting tools like QuickBooks and Excel. The card also comes with built-in security alerts and fraud protection.

- 2% cash back on every purchase

- No preset spending limit

- Relatively low annual fee

- You must pay the card in full after each billing cycle

- Lacks integration with accounting tools

- No ability to set spending limits by category or collect receipts

4. Capital One Venture X Business

The Capital One Venture X Business Card is a pay-in-full charge card with no preset spending limit. It works best for companies whose employees travel often and spend consistently across many categories. Every purchase earns unlimited 2x miles. New cardholders can earn 150,000 bonus miles after spending $30,000 in the first three months.

You also get free employee and virtual cards, customizable spending limits, detailed transaction visibility, and strong security protections. However, teams not traveling frequently may not unlock the full value of the card’s travel benefits.

Plus, the platform doesn’t feature accounting integrations or built-in expense management tools. With a $395 annual fee, it’s best suited for travel-heavy teams that want simple rewards and premium travel perks.

- 2x miles on every purchase

- No preset spending limit

- Additional travel benefits

- May not be ideal if your employees don't travel frequently

- The card must be paid in full each month

- No accounting integrations or expense management features

5. Ramp

Ramp’s corporate charge card focuses on expense management and visibility rather than cash back marketing. They advertise higher credit limits than traditional business credit cards and charge no annual fees, foreign transaction fees, or card replacement fees.

You can issue an unlimited number of physical and virtual employee cards, set detailed spending limits, and monitor transactions in real time. These features make it ideal for managing job-site purchases, foreman-led expenses, and multi-team spend.

Ramp does not advertise traditional rewards or category bonuses, and its full suite of features may be more than smaller businesses need. While the base card is free, costs can increase if you want advanced approvals, deeper accounting integrations, or more sophisticated workflows.

The card must be paid in full each month. Approval is based on business financials rather than personal credit, typically requiring at least $50,000 in a business bank account.

- No card fees

- Advanced spend management tools

- Advertises higher credit limits than other cards

- Advanced approvals and accounting integrations come at a higher cost

- No rewards are advertised

- A full suite of features may be overkill for smaller businesses

6. Bill.com

Bill.com offers a corporate card with a platform for expense management and accounts payable. It’s ideal for construction businesses that want control over spend and vendor payments in one place. There are no card fees. Plus, the card earns 2x rewards on restaurants and hotels, with higher earning rates available depending on how frequently you pay down your balance.

You can redeem rewards for cash back, statement credits, or gift cards, but they come with a few conditions. Rewards on restaurants and hotels are capped after a certain spend level. You won’t earn points at all if you spend less than 30% of your available credit line in a given month.

Bill.com’s AI-powered accounts payable software makes it easy to handle invoice capture, approvals, and payments. You can also integrate it with accounting systems like QuickBooks, NetSuite, Xero, and Sage Intacct. The corporate card can be used alongside BILL’s bill pay tools (available for an additional fee), helping teams manage card spend and vendor payments together.

That said, some customers report mixed experiences with customer support, and the platform may feel more than what smaller teams need.

- No fees to carry or use the card

- Customers on a monthly cycle earn 2x on restaurant and hotel spend

- Bill pay software is available and works with the corporate card for an additional fee

- Some customers (on Trustpilot) report mixed experiences with customer support

- Restaurant and hotel rewards are capped after reaching a spending threshold

- Rewards are only earned when the monthly spend reaches at least 30% of the credit line

7. Chase Sapphire Reserve for Business

The Chase Sapphire Reserve for Business Card is ideal for construction companies that want to extend premium perks to leadership and key employees.

New cardmembers can earn 150,000 bonus points after spending $20,000 in the first three months, worth up to $3,000 toward select flights and hotels booked through Chase Travel. Ongoing travel and business credits can push first-year value past $6,000, offsetting much of the $795 annual fee for the right business.

It’s a pay-in-full charge card with employee cards available at no additional cost and basic account visibility. However, the card focuses more on rewards than expense management. It doesn’t include accounting integrations, receipt capture, or spend-limit controls, and lounge access is limited to the primary cardholder.

- Attractive introductory offer

- 4x on hotels and flights booked direct, 3x on social media and paid marketing

- Significant travel benefits, with lounge access and hotel credits

- Lacks accounting integrations

- No receipt collection feature

- You can’t set spending limits on the card

Choosing Your Construction Company’s Credit Card: Key Considerations

Now that you’ve seen the options, the best credit card for a construction business comes down to fit. Use the factors below to make the final call.

- How crews actually spend: Construction spending is decentralized by design. Fuel, materials, tolls, and emergency repairs happen mid-job, off-route, and often outside planned vendors. Cards with limited acceptance or narrow reward networks force crews to detour, delay work, or use personal cards.

- Built-in controls: You don’t want to see employee misuse and policy drift increase once multiple crews spend independently. The best credit card for construction balances flexibility with guardrails, like employee cards, spend limits, and merchant or category controls, that stop leakage without forcing approvals for every purchase.

- Visibility and job-level tracking: Margins quietly erode when you can’t tie back charges to vehicles, jobs, or projects. Strong construction credit cards provide clean transaction data, receipt capture, and job or project tagging, so finance teams don’t have to reconstruct context at month-end.

- Real reward value: Annual fees, reward caps, minimum usage thresholds, and unused travel credits can erase headline value fast. For many construction businesses, a flat, predictable return or lower-fee card delivers more net value than a premium card with benefits that go unused.

- Workflow compatibility: Manual coding and reconciliation become a bottleneck as transaction volume grows. Cards that integrate cleanly with accounting or project systems reduce errors, speed close, and lower admin cost per dollar spent.

Want to see what the right construction credit card could really save you? Use our calculator to run the numbers and see how small savings add up fast.

Why Pick Coast as Your Construction Company’s Fuel Credit Card

As construction fleets grow, unmanaged fuel spend becomes a problem fast. Coast keeps crews moving while giving the office real-time control and clarity over fuel expenses. Here’s how:

- Wide acceptance: Construction crews don’t fuel at one approved location. Routes change, and jobs run late. Coast lets you fuel anywhere Visa is accepted, while still letting you lock spending to approved categories only.

- Misuse prevention controls: Coast lets you apply spend rules, employee verification, and real-time policy enforcement at the moment of purchase. Plus, telematics data adds another layer by flagging transactions that don’t align with vehicle location, backed by up to a $25,000 annual fuel-fraud guarantee (eligibility and terms apply).

- Real-time visibility: Coast doesn’t let spend sit in limbo until month-end. Every transaction appears instantly with time, location, and amount, so issues surface early. You can review spend by technician, vehicle, or job, without stitching together reports after the money’s already gone.

- Integrations: Receipts, job codes, and custom fields get captured directly from the driver’s phone. Plus, reconciliation stays clean and predictable with direct integrations into QuickBooks, NetSuite, Sage Intacct, and tools like BuildOps or Knowify.

Local construction fleets like KD Construction use Coast to keep spend clean and accountable. You could too.

Apply now and take control of fuel spend.

Construction Credit Card FAQs

1. What’s the best credit card for a small construction business?

Call us biased, but Coast is the best credit card for small construction businesses, especially if you manage vehicles, fuel spend, and field crews. Capital One Spark 2% Cash Plus is a solid option if you want straightforward cash back, while Ramp or BILL make more sense for teams that prioritize expense management over rewards. Chase Sapphire Reserve for Business is best suited for owners or teams with frequent travel needs.

2. Can construction credit cards be used for fuel and job-site purchases?

Some can, yes. Many construction-focused credit and fleet cards are designed to cover everyday business expenses, including fuel, tools, materials, equipment rentals, and other job-site costs. The exact purchase types allowed depend on the card’s terms and how the issuer categorises merchants.

For example, the Coast Visa® commercial card is built as a combined fuel, fleet, and business expense card that works wherever Visa is accepted. It lets construction businesses use the card for fuel at any Visa-accepting gas station, and with flexible controls set by the business, it can also be used for vehicle maintenance, job supplies, and other field-related purchases. You can customise spending rules, including which categories are allowed or blocked, to keep costs aligned with your job-site needs.