Your business is growing and you’re thinking of expanding your fleet. But purchasing multiple vehicles outright can strain your working capital and put you in a major cash flow hole. This is where commercial fleet financing becomes a valuable tool for savvy business owners.

Fleet financing offers a range of options to help you scale your operations without depleting your working capital. It’s about finding smarter ways to acquire the vehicles you need while maintaining financial agility.

In this article, we’ll explore different commercial fleet financing solutions and break down different financing approaches, along with their pros and cons.

Ready to explore how commercial fleet financing can drive your business forward? Let’s get started.

What Is Commercial Fleet Financing?

Commercial fleet financing refers to borrowing money from a lender to purchase fleet vehicles. But fleet financing is more than drawing a loan from a lender.

Commercial fleet financing encompasses a variety of options tailored to meet different business needs and financial situations. Let’s look at these options now.

Types Of Commercial Fleet Financing

There’s no one-size-fits-all solution when you’re looking to finance fleet vehicle purchases.

Every business has different needs. Fortunately, you can choose from a few different financing options.

Let’s first take a look at the four main types of commercial fleet financing:

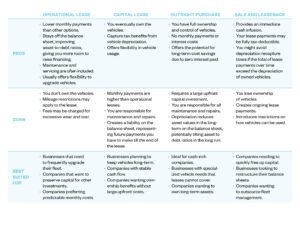

Operational lease: A short-term rental agreement where you use vehicles for a set period, typically 2-5 years. You pay to use the vehicles but don’t own them.

Capital lease: A long-term agreement where you pay the cost of owning the vehicle over time. You’re responsible for maintenance and depreciation. The vehicles appear on your balance sheet, and you usually have the option to buy them at lease-end for a fee.

Outright purchase: Buying vehicles directly with cash. You own the assets immediately, giving you full control but requiring more upfront capital.

Sale and leaseback: You sell your existing fleet to a financing company and then lease it back. This provides an immediate cash infusion while allowing continued use of the vehicles.

Here’s a quick summary of the pros and cons of each fleet financing method.

Operational Lease

Pros

- Lower monthly payments than other options.

- Stays off the balance sheet, improving asset-to-debt ratios, giving you more room to raise financing

- Maintenance and servicing are often included

- Usually offers flexibility to upgrade vehicles

Cons

- You don’t own the vehicles

- Mileage restrictions may apply to the lease

- Fees may be charged for excessive wear and tear

Best suited for

- Businesses that need to frequently upgrade their fleet

- Companies that want to preserve capital for other investments

- Companies preferring predictable monthly costs

Capital Lease

Pros

- You eventually own the vehicles

- Capture tax benefits from vehicle depreciation

- Offers flexibility in vehicle usage

Cons

- Monthly payments are higher than operational leases

- You are responsible for maintenance and repairs

- Creates a liability on the balance sheet, representing future payments you have to make till the end of the lease.

Best suited for

- Businesses planning to keep vehicles long-term

- Companies with stable cash flow

- Companies wanting ownership benefits without large upfront costs.

Outright Purchase

Pros

- You have full ownership and control of vehicles

- No monthly payments or interest costs

- Offers the potential for long-term cost savings due to zero interest paid.

Cons

- Requires a large upfront capital investment

- You are responsible for all maintenance and repairs

- Depreciation reduces asset values in the long-term on the balance sheet, potentially tilting asset to debt ratios in the long run

Best suited for

- Ideal for cash-rich companies

- Businesses with specialized vehicle needs that leases cannot cover

- Companies wanting to own long-term assets.

Sale and Leaseback

Pros

- Provides an immediate cash infusion

- Your lease payments may be fully tax-deductible

- You might avoid depreciation recapture taxes if the total of lease payments over time exceed the depreciation of owned vehicles.

Cons

- You lose ownership of vehicles

- Creates ongoing lease payments

- Introduces restrictions on how vehicles can be used

Best suited for

- Companies needing to quickly free up capital

- Businesses looking to restructure their balance sheets

- Companies wanting to outsource fleet management

How To Apply For Commercial Fleet Financing

Securing the right financing for your fleet can seem complex. Here are the key steps in this process.

Step 1: Determine The Type And Number Of Vehicles You Need

The first step is to thoroughly evaluate your business’s fleet requirements. How many vehicles do you need and what types of fleet vehicles will best serve your operational needs?

Considering factors such as cargo capacity, fuel efficiency, and any specialized features necessary for your industry.

Check Your Credit

Before approaching lenders, it’s crucial to understand your current credit standing. Take the time to review both your business and personal credit scores, as lenders will consider both when evaluating your application for fleet financing.

A strong credit profile can lead to more favorable terms and rates and identifying any issues in advance allows you to address them proactively.

Prepare Financial Statements, Tax Returns, And Business Plans

Collect and organize essential documents such as recent financial statements, tax returns for the past few years, and a detailed business plan that outlines your company’s growth strategy and how the new fleet vehicles fit into it.

Having these documents ready not only streamlines the application process but also demonstrates your preparedness and professionalism to potential lenders.

Research Lenders

Not all lenders are created equal when it comes to commercial fleet financing. Take the time to explore various options, including traditional banks, credit unions, and lenders that specialize in commercial fleet financing.

Each type of lender may offer different advantages, such as competitive rates, industry-specific expertise, or more flexible terms.

Compare Offers

Once you’ve identified potential lenders, reach out to them for detailed quotes. Compare interest rates, loan terms, down payment requirements, and additional fees.

Choose Your Type Of Financing

With offers in hand, it’s time to determine what fleet financing type best suits your needs. Evaluate how each aligns with your cash flow, tax situation, and long-term business strategy.

Remember, the cheapest option isn’t always the best—choose the financing type that offers the right balance of affordability, flexibility, and alignment with your business goals.

Close The Deal

Once you’re satisfied with the terms and have addressed any concerns, it’s time to finalize the deal. Carefully read the entire agreement before signing, ensuring you understand all obligations and commitments.

After signing, coordinate with the lender and vehicle supplier to arrange the delivery of your new fleet vehicles. Be sure to clarify any final details such as delivery timelines, initial payments, and any required documentation for vehicle registration and insurance.

What To Watch Out For When Financing Your Fleet Vehicle

When financing your fleet vehicles, it’s crucial to look beyond the headline rates and terms. Here are key factors to consider to ensure you’re getting a deal that truly benefits your business in the long run:

- Hidden fees: Scrutinize the agreement for any unexpected charges. These can include administration fees, documentation fees, or early repayment penalties that may significantly increase costs

- Mileage restrictions: Check if there are limits on how many miles you can drive. Exceeding these limits can result in hefty charges, so make sure mileage limits align with your business needs

- Maintenance responsibilities: Clarify who is responsible for vehicle maintenance and repairs. Some agreements include maintenance, while others leave it entirely to you, affecting your total cost of ownership

- Early termination penalties: Understand the costs of ending the agreement before its term. Business needs can change, and you want to avoid being locked into punitive terms

- Residual value assumptions: For leases, verify that the projected value of the vehicle at the end of the term is realistic. An inflated residual value can lead to unexpected costs or obligations at the end of the lease

- Interest rates: Compare interest rates and check whether they’re fixed or variable. Variable rates might start lower but could increase over time, impacting your budget

- Tax implications: Consider how different financing methods affect your tax situation. Some options may offer more favorable tax treatment than others, potentially saving your business money

- Vehicle flexibility: Check if your agreement allows adding or removing vehicles as your needs evolve. Flexibility is crucial for managing your fleet efficiently

- Insurance requirements: Be aware of any fleet insurance terms the lender needs. Some may mandate higher coverage levels, affecting your insurance costs.

Your Fleet Needs The Right Financing—And Software

Financing your fleet is the first step in optimizing your business operations. The costs you incur at this stage will define the efficiency of your fleet management program.

However, effective fleet management also needs the right software. Essential tools like a smart gas card, telematics, and fleet management software supercharge fleet management. Link your smart gas card to telematics and you’ll automate several fleet management tasks.

Integrate both to a fleet management platform and you’ll gain a bird’s eye view of your fleet’s performance. Curious about what a smart gas card can do for your fleet?

Check out how Coast’s smart Visa fuel cards save you 2-10c per gallon and simplify fleet expense management.